Gold steady, Brent on track to 3rd daily gain

- Gold holds firm near $3,406

- Fed seen cutting rates 25 bps in September

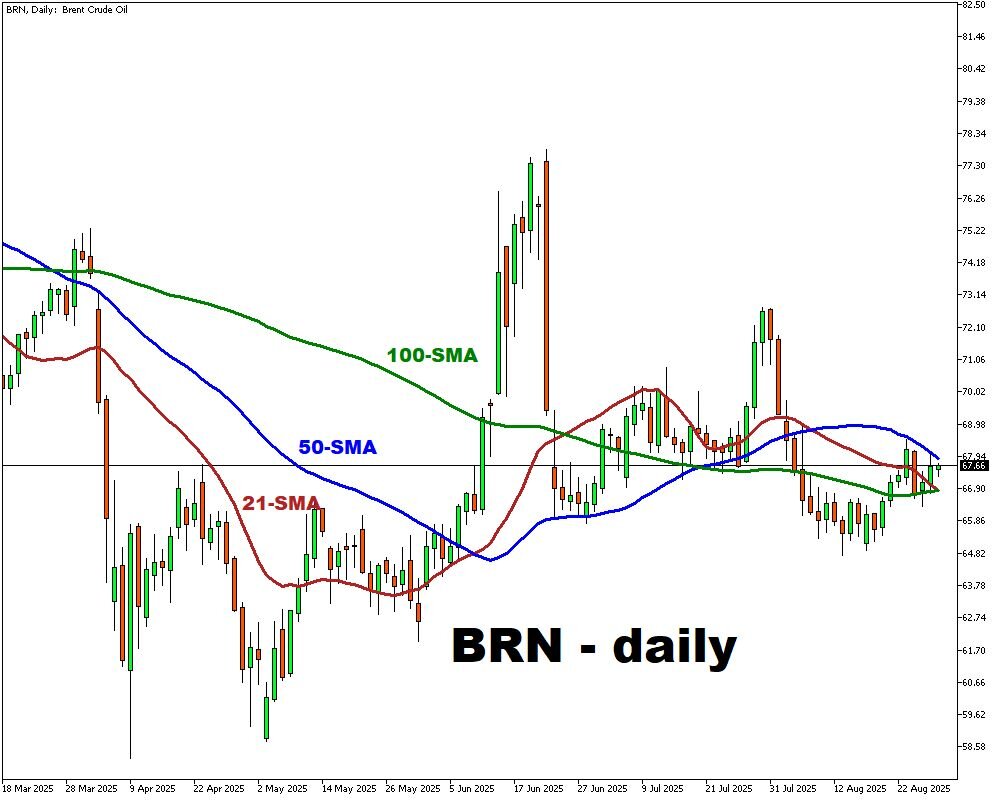

- Brent near $67, demand may be easing post-Labor Day

- OPEC+ supply, geopolitics keep oil uncertain

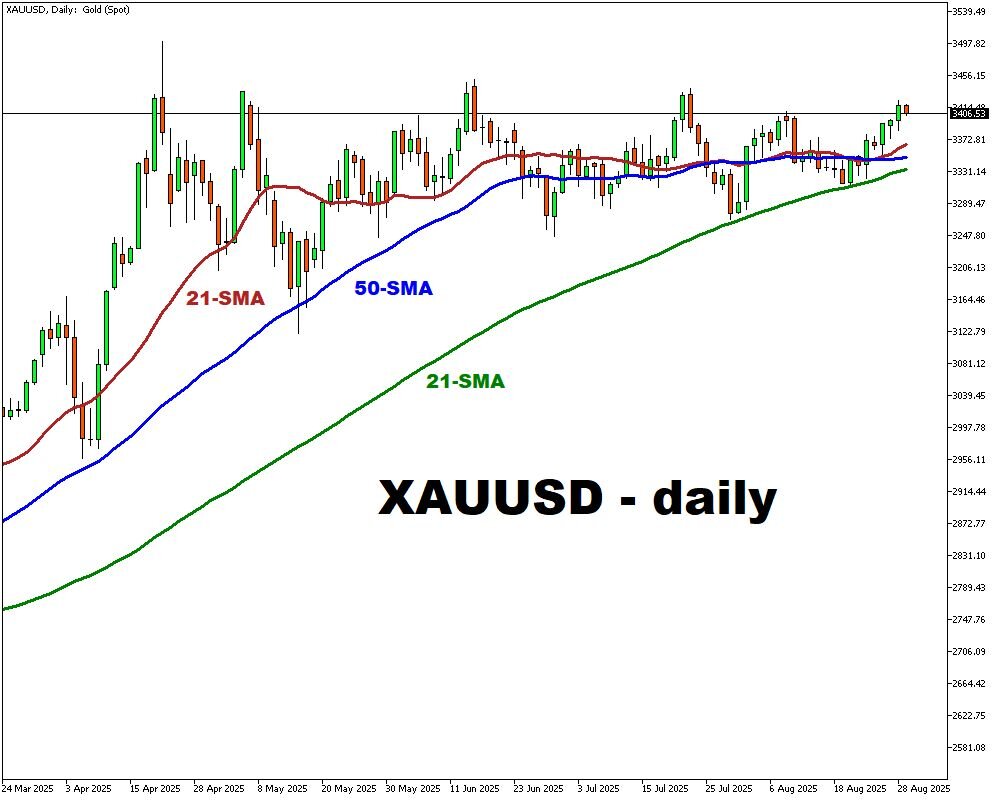

Gold (XAUUSD)

Gold prices held firm around $3,406 per ounce on Friday, staying close to their highest mark in over a month.

The metal is heading for a second straight week of gains, supported by a softer U.S. dollar and a persistent bid for safe-haven assets.

Investor sentiment has been shaped largely by expectations for Federal Reserve policy. With political pressure mounting for a faster easing cycle, markets are pricing in a 25-basis point rate cut in September (85.2% probability).

Fed Governor Christopher Waller reinforced this view, saying he “fully expects” further reductions to guide policy closer to neutral, aligning with remarks from other Fed officials.

At the same time, markets are watching Friday’s release of the U.S. personal consumption report, expected to be unchanged from the previous 0.3% (Core PCE). Despite this, gold remains buoyed by its role as a hedge against both policy uncertainty and price instability.

For August, the metal is on course for its strongest monthly performance since April.

Brent Crude

Brent hovers near $67, eyeing 3rd daily gain despite demand and supply risks.

Risks are looming as the U.S. driving season winds down after Labor Day, with fuel consumption projected to ease.

The IEA recently forecasted that global supply is likely to outpace demand in the coming quarters, particularly as OPEC+ continues to restore idle production capacity.

These concerns have pushed Brent toward its first monthly loss in four. Nonetheless, geopolitical risks remain a counterweight.

India’s stance on Russian imports also remains a swing factor, as analysts anticipate September shipments to rise despite U.S. pressure.

Overall, Brent is caught between bearish fundamentals and ongoing geopolitical uncertainty.